As we move into an economy governed by a new president in 2017, tax strategies will inevitably change for future tax years. Fortunately, this past year brought positive trends, such as increased GDP output, unemployment claims at a 43-year low, and more, meaning our next president will inherit a more robust economy. Though we won’t know precisely what the 2018 tax environment will be until after President-Elect Trump takes office, you can still create efficiency in your tax planning this year.

What’s in store for 2017?

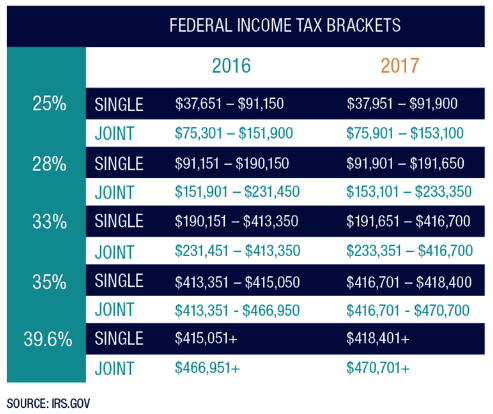

The IRS recently announced its inflation adjustments for the 2017 tax year, which we summarize below.

Actions You Can Take

Contribute Maximum Amount to Retirement Accounts

You have until April 18, 2017, to contribute your maximum amounts to your IRA accounts. (Dates may vary by state.) The sooner you contribute the money, the sooner the amount can start growing tax deferred.

Making deductible contributions also reduces your taxable income for the year. In 2016 and 2017, you can contribute a maximum of $5,500 per person, plus an extra $1,000 if you’re 50 and older. You can split this limit between a traditional IRA and a Roth IRA, if you desire; the combined limit is still $5,500, or $6,500 if you are over 50.

Before you act on any strategies, we encourage you to consult with your tax professional about the options that are right for you.

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, member FINRA/SIPC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Bush Wealth Management and LPL Financial are separate entities.